filmov

tv

how to analyse garch eviews

0:08:01

EViews: (3 of 3) How to Estimate ARCH, GARCH, EGARCH & GJR-GARCH(or TGARCH) Models

0:02:35

GARCH-in-mean model - Eviews

0:09:23

Video 14 Estimating and interpreting an EGARCH (1,1) model on Eviews

0:07:09

(EViews10) - How to Estimate ARCH Models #arch #timeseries #volatility #modeling #econometrics

0:10:45

(EViews10): How to Estimate Threshold GARCH (GJR-GARCH) #garchm #tgarch #egarch #gjr-garch

0:03:43

Dynamic Conditional Correlation DCC GARCH Model in Eveiws

0:05:51

(EViews10): ARCH vs. GARCH Models (Estimations) #garch #arch #parsimony #volatility

0:14:10

Praktikum Ekonometrika II - Analisis ARCH/GARCH di EViews

0:19:56

Econometrics228: ARCH GARCH Models; TGARCH and EGARCH

0:50:34

ATAL FDP - Research in Finance Using Eviews - Modeling Volatility using GARCH

0:07:47

Eviews. Modelos arch

0:03:45

GARCH and EGARCH models - Eviews

0:08:56

Unit root in GARCH using Eviews

0:17:05

17. Auto Regressive Conditional Heteroskedasticity (ARCH) Model in EViews 12 || Dr. Dhaval Maheta

0:35:33

RFM 2020 Lecture 5(4) Eviews Tutorial for Lecture 5 (GARCH-in-mean models)

0:02:23

Multivariate GARCH DCC Estimation

0:12:38

24.ARCH and GARCH models, using EViews (Part-1)||Example from Financial Time Series

0:19:09

25. Estimating ARCH and GARCH models using EViews (Part-2)||ARCH, GARCH, GARCH-M, TGARCH, EGARCH

0:04:40

Video 9 How to estimate an ARCH(q) model (part 3) as well as interpret the results on Eviews

0:04:14

Spill over effect: Using GARCH (1,1) model on eviews

0:16:00

ARCH et GARCH

0:11:08

Tutorial Estimasi ARCH/GARCH Dengan Eviews

0:02:47

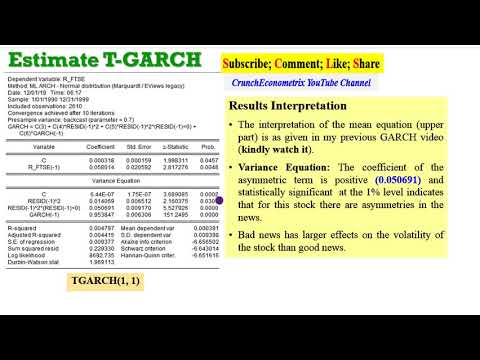

Estimating TGARCH or GJR GARCH models in Eviews

0:11:01

13 ARCH and GARCH practical with interpretation, Econometrics

Назад

Вперёд

0:08:01

0:08:01

0:02:35

0:02:35

0:09:23

0:09:23

0:07:09

0:07:09

0:10:45

0:10:45

0:03:43

0:03:43

0:05:51

0:05:51

0:14:10

0:14:10

0:19:56

0:19:56

0:50:34

0:50:34

0:07:47

0:07:47

0:03:45

0:03:45

0:08:56

0:08:56

0:17:05

0:17:05

0:35:33

0:35:33

0:02:23

0:02:23

0:12:38

0:12:38

0:19:09

0:19:09

0:04:40

0:04:40

0:04:14

0:04:14

0:16:00

0:16:00

0:11:08

0:11:08

0:02:47

0:02:47

0:11:01

0:11:01